Deposit insurance is a crucial aspect of the financial sector as it serves as a safety net for depositors, protecting their money in the event of a bank failure or insolvency. Deposit insurance ensures that depositors do not lose their savings in case of bank closure or bankruptcy. Deposit insurance is important because it promotes confidence in the financial system, which is crucial for the stability and growth of the economy.

Financial innovation is essential in deposit insurance because it enhances the effectiveness of deposit insurance schemes. Financial innovation in deposit insurance involves the development and implementation of new policies, processes, and technologies that improve the efficiency and effectiveness of deposit insurance schemes. Financial innovation helps to address challenges and improve deposit insurance schemes, making them more effective in protecting depositors’ funds.

In this article, we will explore the importance of financial innovation in deposit insurance, with a focus on the African continent. We will examine how financial innovation in deposit insurance has helped policyholders, and what other things/activities need to be done by the industry to help boost this.

The importance of deposit insurance

Deposit insurance is important for several reasons. Firstly, it promotes confidence in the financial system. When depositors are confident that their money is safe, they are more likely to keep their savings in the bank. This helps to maintain the stability and growth of the economy by ensuring the smooth functioning of the financial system.

Secondly, deposit insurance provides protection for small depositors who cannot afford to lose their savings. In many developing countries, small depositors make up the majority of the population. Deposit insurance provides a safety net for these depositors, protecting their savings in case of a bank failure or insolvency.

Thirdly, deposit insurance helps to prevent bank runs. When depositors lose confidence in a bank, they may rush to withdraw their savings. This can lead to a bank run, which can quickly spread to other banks and cause a systemic banking crisis. Deposit insurance provides a safety net for depositors, reducing the likelihood of bank runs.

Finally, deposit insurance helps to promote financial inclusion. When depositors know that their money is safe, they are more likely to use formal financial services, which can help to promote financial inclusion and economic growth.

Financial innovation in deposit insurance

Financial innovation in deposit insurance involves the development and implementation of new policies, processes, and technologies that improve the efficiency and effectiveness of deposit insurance schemes. Financial innovation helps to address challenges and improve deposit insurance schemes, making them more effective in protecting depositors’ funds.

One example of financial innovation in deposit insurance is the use of mobile technology. In many African countries, mobile phones are more widely used than traditional banking services. Mobile money services have become popular in countries such as Kenya, Uganda, and Tanzania. These services allow depositors to send and receive money, pay bills, and access other financial services using their mobile phones. Mobile money services have enabled more people to access financial services, including deposit insurance, which has helped to promote financial inclusion.

In Kenya, the Kenya Deposit Insurance Corporation (KDIC) is responsible for insuring bank deposits in Kenya. However, in 2010, the Central Bank of Kenya (CBK) and the Communications Authority of Kenya (CAK) signed a memorandum of understanding to promote the use of mobile money services and encourage innovation in the sector. This led to the introduction of new regulations that allowed non-bank entities, such as mobile network operators, to offer financial services, including deposit-taking.

In 2012, Safaricom, the leading mobile network operator in Kenya, launched a savings and loan product called M-Shwari in partnership with the Commercial Bank of Africa (CBA). M-Shwari allowed M-Pesa customers to save and borrow money using their mobile phones. In 2014, the Kenya Deposit Insurance Corporation (KDIC) announced that it would insure deposits held in M-Shwari accounts up to a maximum of Kshs. 100,000 (approximately USD 1,000) per depositor.

Another example of financial innovation in deposit insurance is the use of risk-based pricing. Risk-based pricing is a pricing strategy where the premium charged for deposit insurance is based on the risk of the bank. Banks that are considered to be more risky pay higher premiums than banks that are considered to be less risky. Risk-based pricing encourages banks to manage their risks better, which can reduce the likelihood of bank failures and insolvencies. It also ensures that deposit insurance schemes are financially sustainable, as banks that pose a higher risk to the scheme are required to pay higher premiums.

Deposit insurance schemes in Africa, such as the Deposit Guarantee Fund (DGF) in some countries, provide protection to depositors in the event of bank failures. While specific pricing structures and methods used to determine deposit insurance premiums may vary depending on the country and regulatory authority, it is important to note that risk-based pricing is a common practice in the insurance industry.

Under a risk-based pricing structure, premiums are adjusted to reflect the level of risk associated with insuring a particular policy. This incentivizes banks to manage their risks better, which in turn reduces the likelihood of bank failures and insolvencies. While I cannot confirm the specific information mentioned earlier regarding the DGF implementing risk-based pricing, it is possible that some deposit insurance schemes in Africa have adopted this practice.

Another example of financial innovation in deposit insurance is the use of technology to improve the efficiency of deposit insurance schemes. In many African countries, traditional banking services are not always accessible, particularly in rural areas. This can make it difficult for deposit insurance schemes to reach all depositors, particularly those in remote areas.

One example of this is the implementation of online platforms by deposit insurance schemes to allow depositors to file claims and check the status of their deposits. The Kenya Deposit Insurance Corporation (KDIC) has implemented an online platform that allows depositors to file claims and check the status of their deposits, increasing access to deposit insurance services.

Challenges to financial innovation in deposit insurance

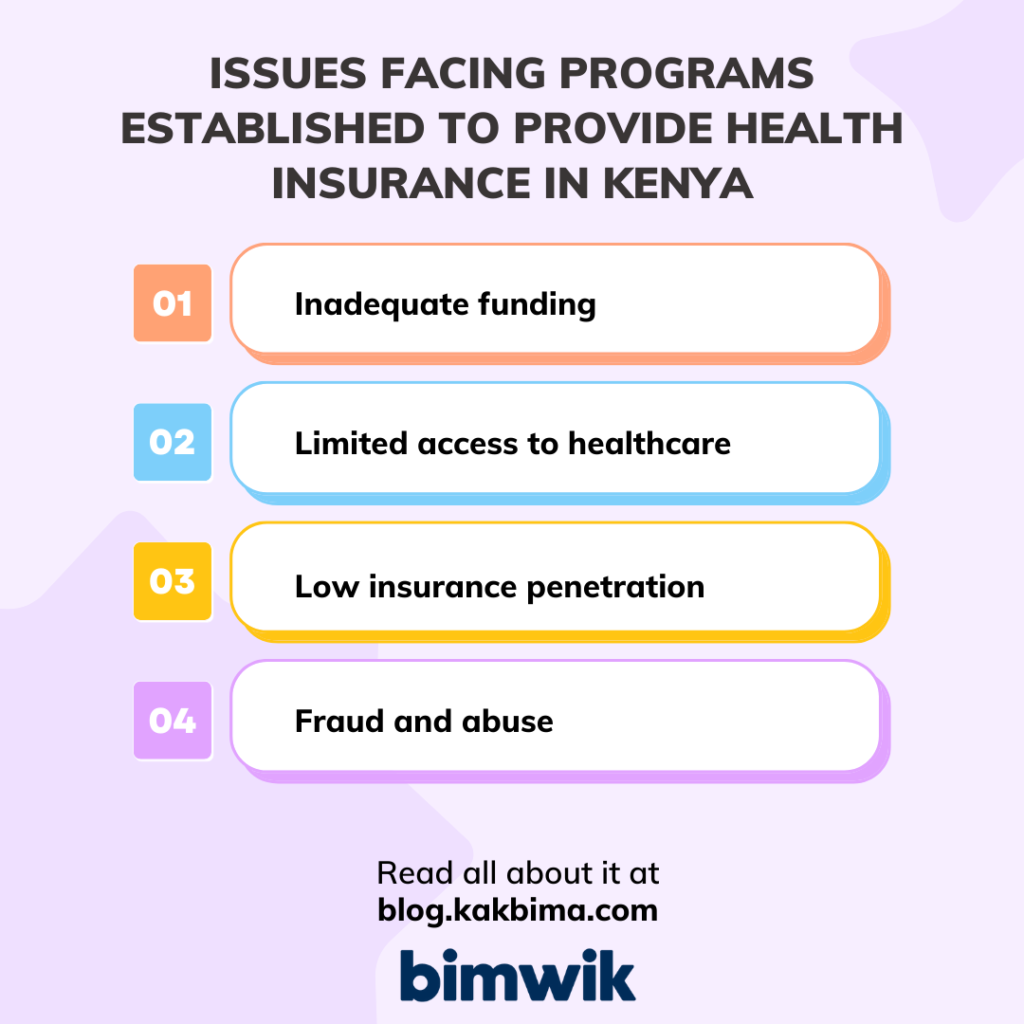

While financial innovation in deposit insurance has many benefits, there are also several challenges to its implementation. One of the challenges is the lack of regulatory and legal frameworks to support financial innovation. Many African countries have outdated legal and regulatory frameworks that do not support financial innovation. This can make it difficult to implement new policies, processes, and technologies that can improve deposit insurance schemes.

Another challenge is the lack of technical expertise and capacity. Financial innovation in deposit insurance requires technical expertise and capacity, particularly in the areas of information technology, risk management, and data analytics. Many African countries lack the technical expertise and capacity to implement financial innovation in deposit insurance effectively.

Finally, there is a lack of awareness and understanding of the benefits of financial innovation in deposit insurance among policymakers, regulators, and stakeholders. Many policymakers, regulators, and stakeholders are not aware of the benefits of financial innovation in deposit insurance, which can make it difficult to implement new policies, processes, and technologies that can improve deposit insurance schemes.

Financial innovation is essential in deposit insurance because it enhances the effectiveness of deposit insurance schemes. Financial innovation in deposit insurance involves the development and implementation of new policies, processes, and technologies that improve the efficiency and effectiveness of deposit insurance schemes. Financial innovation helps to address challenges and improve deposit insurance schemes, making them more effective in protecting depositors’ funds.

In Africa, financial innovation in deposit insurance has helped to promote financial inclusion, reduce the likelihood of bank failures and insolvencies, and improve the efficiency of deposit insurance schemes. However, there are also several challenges to the implementation of financial innovation in deposit insurance, including the lack of regulatory and legal frameworks, technical expertise and capacity, and awareness and understanding of the benefits of financial innovation.

To address these challenges, policymakers, regulators, and stakeholders need to work together to develop and implement legal and regulatory frameworks that support financial innovation in deposit insurance. They also need to invest in building technical expertise and capacity in the areas of information technology, risk management, and data analytics. Finally, they need to raise awareness and understanding of the benefits of financial innovation in deposit insurance among policymakers, regulators, and stakeholders. By doing so, they can improve the effectiveness of deposit insurance schemes and promote financial inclusion and economic growth in Africa.